On Contract

Ta-Nehisi Coates's The Case For Reparations explains that racial differences in America are the product of systematic economic exclusion and exploitation, from slavery and Reconstruction to Jim Crow and redlining. It has been a big influence on my thinking: I presented the collection in which it sits, We Were Eight Years in Power, in my first seminar at Oxford.

The argument is economic: black Americans are poor because they were excluded, by racist policy choices, from opportunities that made white Americans rich. Perhaps the greatest of those opportunities was the post-WW2 housing market, from which most black Americans were excluded.

It’s well known that this exclusion was caused by redlining; but Coates’ essay provides two further mechanisms for inequality: that FHA loans constituted a "bounty" from which black Americans were excluded, and that contracts for deed, to which black home buyers unable to secure a traditional mortgage resorted, were uniquely predatory.

In this essay, I'll suggest an alternative interpretation. Contracts for deed are a normal financial product, still common on both sides of the Atlantic; and Coates drastically underestimates the effects of the unduly restrictive lending environment of the 1950s and 1960s. With that said, here’s how Coates frames the story:

In 1961, Ross and his wife bought a house in North Lawndale, a bustling community on Chicago’s West Side. North Lawndale had long been a predominantly Jewish neighborhood, but a handful of middle-class African Americans had lived there starting in the ’40s. The community was anchored by the sprawling Sears, Roebuck headquarters. North Lawndale’s Jewish People’s Institute actively encouraged blacks to move into the neighborhood, seeking to make it a “pilot community for interracial living.” In the battle for integration then being fought around the country, North Lawndale seemed to offer promising terrain. But out in the tall grass, highwaymen, nefarious as any Clarksdale kleptocrat, were lying in wait.

Three months after Clyde Ross moved into his house, the boiler blew out. This would normally be a homeowner’s responsibility, but in fact, Ross was not really a homeowner. His payments were made to the seller, not the bank. And Ross had not signed a normal mortgage. He’d bought “on contract”: a predatory agreement that combined all the responsibilities of homeownership with all the disadvantages of renting—while offering the benefits of neither. Ross had bought his house for $27,500. The seller, not the previous homeowner but a new kind of middleman, had bought it for only $12,000 six months before selling it to Ross. In a contract sale, the seller kept the deed until the contract was paid in full—and, unlike with a normal mortgage, Ross would acquire no equity in the meantime. If he missed a single payment, he would immediately forfeit his $1,000 down payment, all his monthly payments, and the property itself.

The men who peddled contracts in North Lawndale would sell homes at inflated prices and then evict families who could not pay—taking their down payment and their monthly installments as profit. Then they’d bring in another black family, rinse, and repeat. “He loads them up with payments they can’t meet,” an office secretary told The Chicago Daily News of her boss, the speculator Lou Fushanis, in 1963. “Then he takes the property away from them. He’s sold some of the buildings three or four times.”

Ross had tried to get a legitimate mortgage in another neighborhood, but was told by a loan officer that there was no financing available. The truth was that there was no financing for people like Clyde Ross. From the 1930s through the 1960s, black people across the country were largely cut out of the legitimate home-mortgage market through means both legal and extralegal. Chicago whites employed every measure, from “restrictive covenants” to bombings, to keep their neighborhoods segregated.

Their efforts were buttressed by the federal government. In 1934, Congress created the Federal Housing Administration. The FHA insured private mortgages, causing a drop in interest rates and a decline in the size of the down payment required to buy a house. But an insured mortgage was not a possibility for Clyde Ross. The FHA had adopted a system of maps that rated neighborhoods according to their perceived stability. On the maps, green areas, rated “A,” indicated “in demand” neighborhoods that, as one appraiser put it, lacked “a single foreigner or Negro.” These neighborhoods were considered excellent prospects for insurance. Neighborhoods where black people lived were rated “D” and were usually considered ineligible for FHA backing. They were colored in red. Neither the percentage of black people living there nor their social class mattered. Black people were viewed as a contagion. Redlining went beyond FHA-backed loans and spread to the entire mortgage industry, which was already rife with racism, excluding black people from most legitimate means of obtaining a mortgage.

“A government offering such bounty to builders and lenders could have required compliance with a nondiscrimination policy,” Charles Abrams, the urban-studies expert who helped create the New York City Housing Authority, wrote in 1955. “Instead, the FHA adopted a racial policy that could well have been culled from the Nuremberg laws.”

In the first years of the twentieth century, credit was hard to come by. Per the delightful little enchiridion History of Mortgage Finance With an Emphasis on Mortgage Insurance, until 1916, "in almost every state in the nation, state law restricted banks and insurance companies to a maximum loan of 50 percent of the appraised value of a home, and limited the maximum term of the loan to five years for a national bank and 10 years for an insurance company."

By contrast, today most first-time buyers put down 6-8% for a thirty-year mortgage - 85% less money over a 3x longer term. As real estate prices grew and speculators crowded - Florida saw a remarkable cycle between 1925 and 1926 - credit expanded, and mortgage insurance came with it.

Mortgage insurance protects the lender from losses caused by a default. It's a funny kind of insurance, because the borrower pays the premium while the lender receives the benefit. Mortgage insurance is a social good - it expands credit, and helps poor people get loans. As a 2023 report from the Housing Finance Policy Centre states, "during the past 66 years, the private mortgage insurance (PMI) industry has enabled homeownership for more than 38 million borrowers who lack sufficient funds for a 20 percent down payment on a conventional mortgage."

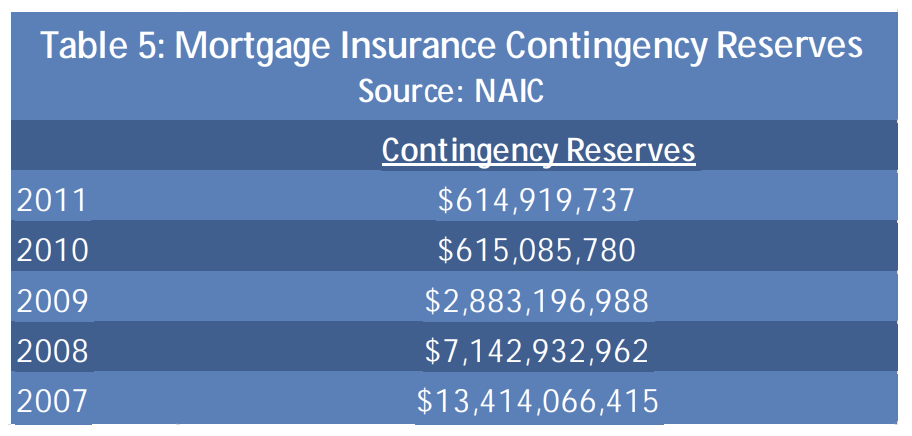

New York State made private mortgage insurance (PMI) legal in 1904,; by 1930, there were 50 companies offering private mortgage insurance in New York State alone. The growth in their reserves - and liabilities - can be seen in the table below.

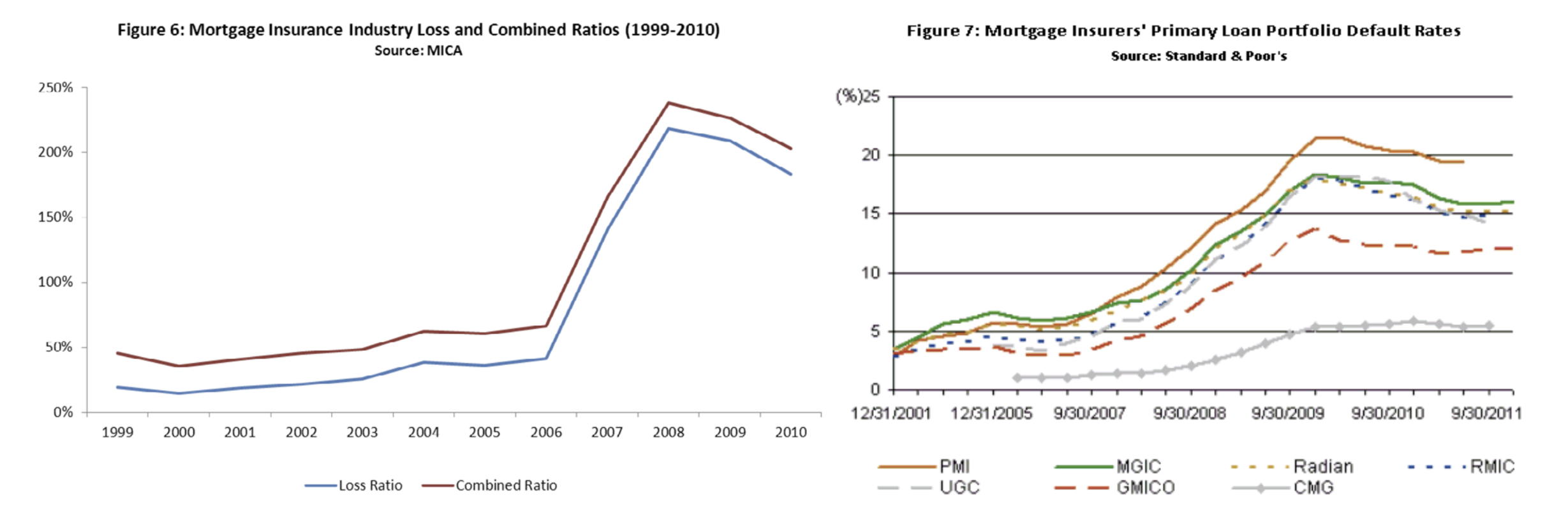

Mortgage insurance looks a little like reinsurance, and so it should have an incredibly good loss ratio in normal times, because the bad times are really bad. To quote a 2013 article from the Basel Committee on Banking Supervision,

The events of the last few years, particularly those in the global financial crisis that began in 2007, indicate that mortgage insurance is subject to significant stress in the worst tail events. In the worst cases, failure of a mortgage insurer may occur leading to resolution of the insurer, whereby some of the most extreme tail risk may revert to the lender at the very time that the insurance would be most needed, potentially creating systemic risk.

The Depression was one of these times.

By 1933, per the US Foreclosure Network, “a staggering 40 to 50 percent of all mortgages in the United States were in default, leading nearly 275,000 people into foreclosure as compared to 68,000 in 1926”. 80% of outstanding real estate bonds in 1935 were in default, and recovery on these bonds averaged just over 50 cents on the dollar.

In August 1933, the Department of Insurance seized 18 mortgage guarantee companies for liquidation; by the end of 1933, every single private mortgage insurer, both in New York State, and in the wider United States, was gone. Per The Anatomy of a Residential Mortgage Crisis: A Look Back to the 1930s:

These [18 private mortgage insurance] companies together had sold $1 billion of insured whole mortgage loans and $0.8 billion of participation certificates on loans that were held in trust accounts; these certificates were held by more than 200,000 investors. The Department of Insurance found that $1.1 billion of guaranteed mortgages were in default... The public investigation of the mortgage guarantee industry in New York revealed that companies had violated underwriting standards, substituted bad loans for performing mortgages in their mortgage pools, and maintained inadequate guarantee funds to support their insurance policies... In 1937 the Joint Legislative Committee to Investigate the Guaranteed Mortgage Situation concluded 'that the business of guaranteeing mortgages should be prohibited entirely'.

PMI would not return until 1956, with insurers subsequently enjoying a profitable run of results until the 1980s. In the period 1953 to 1963, mortgage delinquency was under 1.3%; by the 1990s, this had stabilised at 2.5%, peaking at over 10% in the financial crisis.

To make the point about bad times - The members of the Mortgage Insurance Companies of America had an average loss ratio of 36% in 2005. By 2008, it was 218%. The aggregate contingency reserves of the entire industry shrank by more than 95 percent between 2007 and 2011.

It was in this context––the expansion of credit from 1916 to 1929, and the catastrophic losses that ensued––that the economic policy of the New Deal was forged.

Marriner Stoddard Eccles was one of the architects of the New Deal. After saving his Utah bank holding company from the Crash, in November 1934, he was appointed 7th Chair of the Federal Reserve by FDR, and would hold that office until 1948. In 1956, he outlined his philosophy as follows:

I felt that in a depression the proper role of government should be that of generating a maximum degree of private spending through a minimum amount of public spending. This was the basic justification for deficit spending... I wanted the housing program to be private in character, with all financing done on the grass-roots level by credit institutions of a community for the individuals who lived there. I felt that every kind of credit agency in the country with idle money on its hands should have a right to participate in the financing program.

The goal, then, was to do a lot with a little. His "housing program" was not a “bounty”: it was the bare minimum that Eccles and his colleagues felt would keep the financial and construction industry afloat - to prime the pump, so to speak. Crucially, state intervention in the home lending market was actually profitable for the FHA.

That same attitude was evident in the first Depression-era attempt to intervene in the home lending market: Hoover's Federal Home Loan Bank (FHLB), launched in 1932. 41,000 people applied for an FHLB loan in the first two years; just three were approved. Subsequent programs were larger, but scarcely more generous.

The FHA was established by FDR's June 1934 National Housing Act. From 1934 through 1954, the FHA insured 2.9 million mortgages, but only 9,253 properties were foreclosed - a rate of 0.3 percent. The net loss to the fund over twenty years was $3 million, or about $562 per property. The loss ratio was 0.6 percent. From 1935 to 1957, the FHA's MMI Fund reported ~$1.31 billion in gross income from premiums and investments, while operating expenses were ~$464 million.

So, we have a paradox.

FHA mortgage insurance was not a subsidy - it was profitable for underwriters (the government)

There was excess demand for this insurance

This should have been a win-win; why didn't the government sell more insurance? And why did private capital not rush in to fill the gap? What prevented private mortgage insurance being provided sooner and more broadly, on equal or better terms to the FHA?

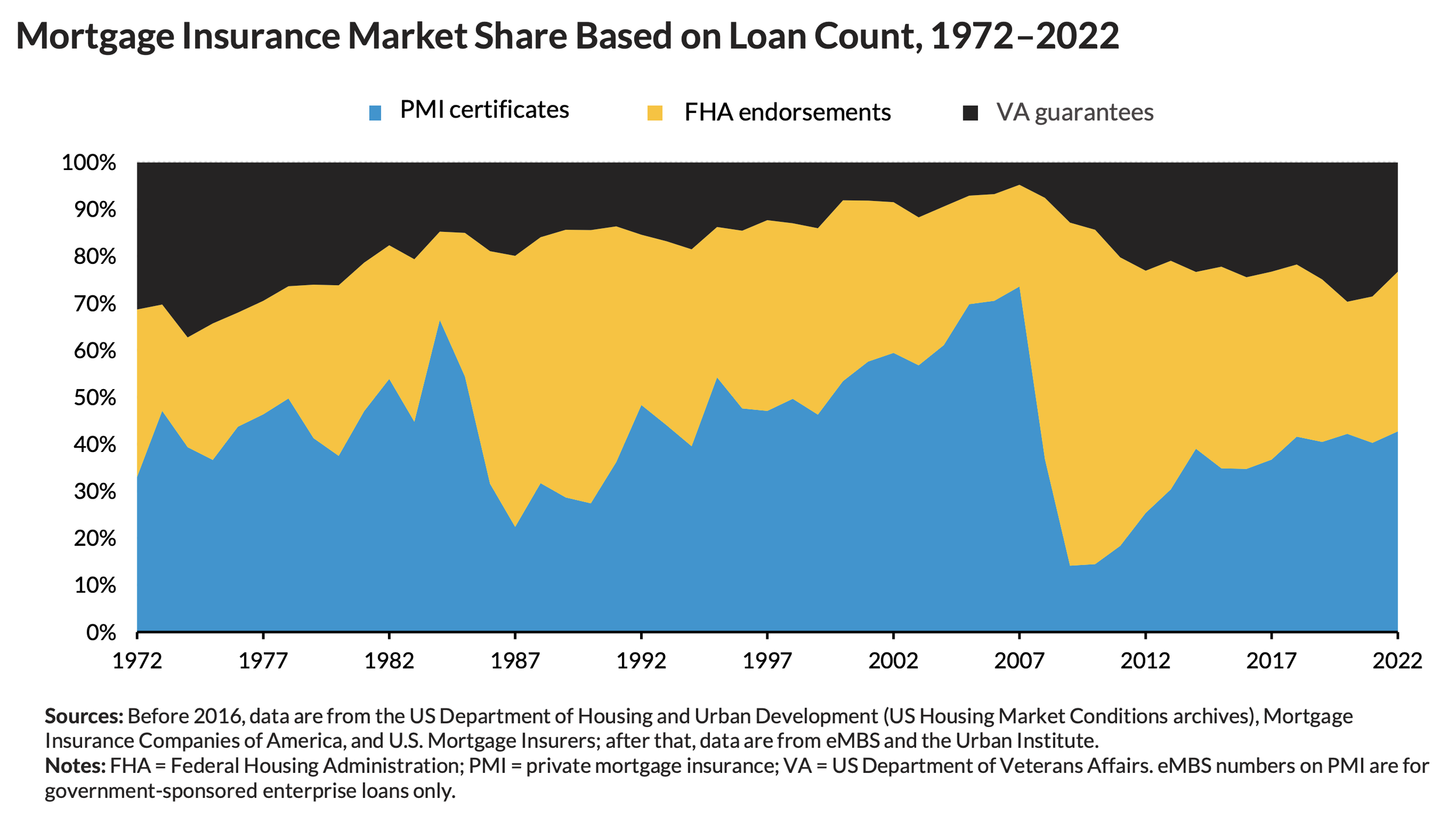

Ironically, once PMI was broadly legal (from 1961 onwards), it rapidly gained market share; as the graph below demonstrates, the period from the 1930s to the late 1950s was anomalous for not having mortgage insurance. The decision to restrict mortgage insurance restricted the supply of credit, creating excess demand.

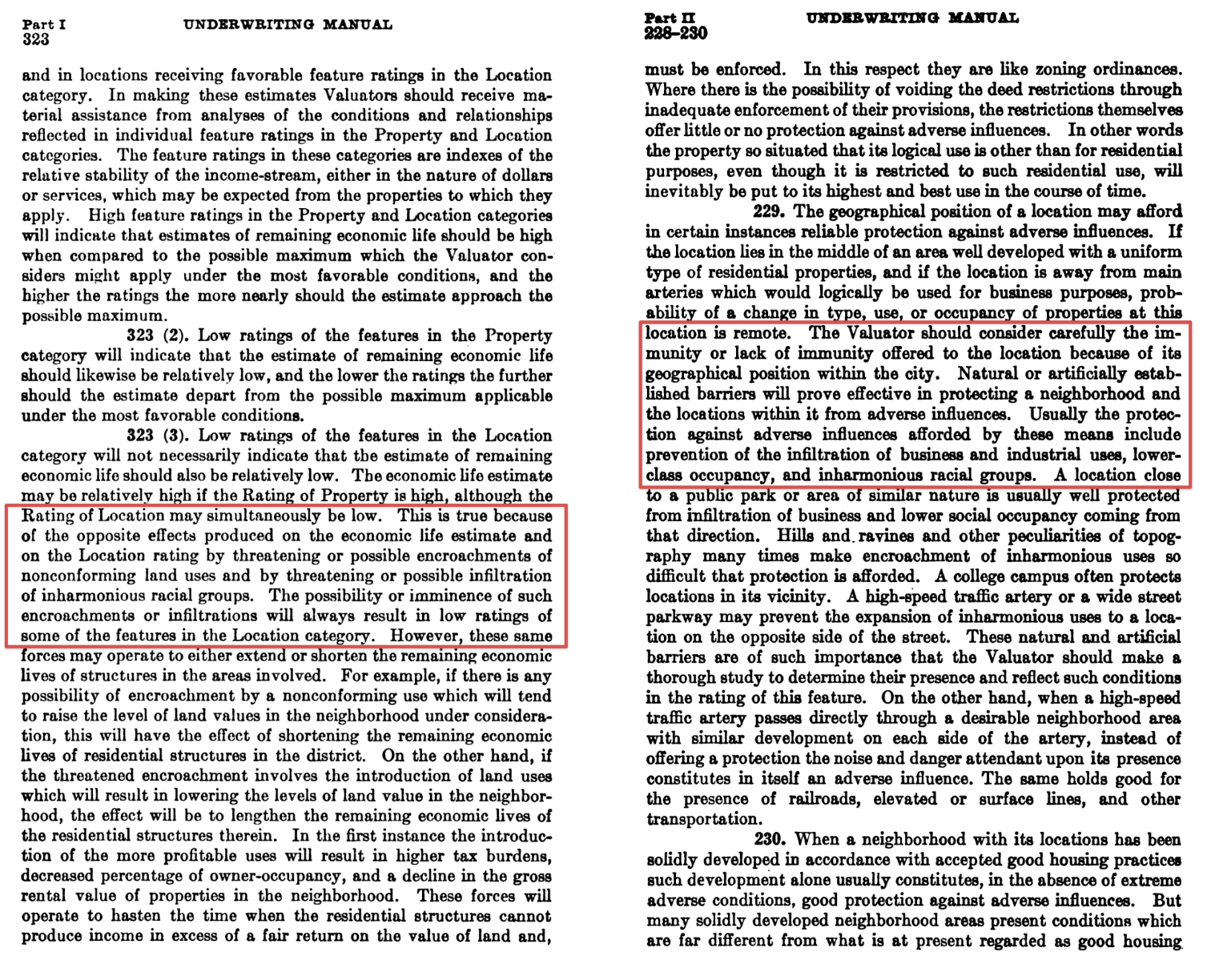

The FHA handled that excess demand by rationing: refusing mortgages to what they saw as the most high-risk portion of society, and making that adjudication in a racist way. Neighbourhoods with “inharmonious racial groups” were penalised, creating segregation. This was redlining - and it was defined by the FHA’s April 1936 underwriting manual, operating under Title II, Section 203 of FDR’s 1934 National Housing Act.

In this case, the FHA's advice produced the social damage that Coates chronicles so evocatively. There's a good line in Patrick McKenzie's Bits About Money essay on Minnesota daycare fraud about how America has reacted to these 1930s handbooks:

One of the first things you learn as a data analyst is zip codes are extremely probative and you are absolutely not allowed to use them. The American system remembers the experience of redlining and has forbidden the financial industry from ever doing it again; the industry mostly respects that.

Perhaps it was the case that the marginal risk was unprofitable; the FHA's redlining was successful on its own terms. But I suspect that the FHA was not profit-maximising, and instead that the answer was cultural and technological. Even though returns were good, financial markets and regulators, scarred by the Depression, were too cautious.

Perhaps(although I can't substantiate this) the scale of the opportunity was concealed by lack of technology: pre-Bloomberg, it would have been harder to quantify. I'd be fascinated to read something about the discussions between insurance executives, lobbyists, and lawmakers in the run-up to the relaunch of of the PMI market in 1956; what were the dissenting voices, and how persuasive were they?

It's easy to criticise America for being overly financialised, but when you don't have a sophisticated credit market that's looking for yield everywhere it possibly can, you get wannabe homeowners that find loans. If they had lived in a time and a market able to support Bilt, Clyde Ross and the North Lawndale market would have been better served.

To summarise, then: The New Dealers were not pantomime racist villains, but rather actuaries and bankers who had just lived through the worst financial catastrophe in American history, and were *terrified* of it happening again. The FHA and FHLB were extraordinarily conservative––far too conservative––because they were created in the aftermath of a terrible crash, but then operated in good times. But they were neither a giveaway nor a bounty.

With this more detailed understanding of the post-Depression credit market in hand, it now pays to turn to the structure of buying "on contract". Coates presents these mortgages as uniquely harmful, sold by "highwaymen" in the "long grass", which should be consigned to history like segregated buses.

But contracts for deed are normal. From 2005 to 2009, approximately 5% of owner-occupied households in the U.S. bought “on contract”. Since contract for deed lending provides additional protections to sellers, it's faster and cheaper for borrowers at the low end of the market.

To illustrate the point: in 2015, there were more contracts for deed than mortgages filed publicly in Detroit: 2,177 vs. 2,023. While these numbers are just a subset of the total, since there is no requirement to publicly disclose mortgages or contracts for deed, it's clear that low-income Americans often still buy on contract. And a story from Akers and Seymour's 2018 ‘Instrumental exploitation: Predatory property relations at city's end' provides further colour:

In one case, for example, a contract for deed borrower agreed to pay $43,003 for the home with an 11% interest rate. The monthly payment was $400 for principal and interest and $170 for property taxes. The borrower was eventually evicted and lost all equity in the home, including approximately $12,000 in payments.

This story mirrors that of Clyde Ross; as such, Ross’s plight was not the product of racism; it was the product of poverty.

Funnily enough, the British car finance ecosystem is dominated by a structure very similar to the contract for deed: PCP, or Personal Contract Purchase. In 2016, 87% of all new cars bought on finance in the UK were bought on PCP.

Here's how it works. You pay a deposit, then make monthly payments for three or four years. At the end, you face a choice: pay a large "balloon payment" (typically around 30% of the car's original value) to actually own the car, hand it back and walk away, or (the most common option) use any remaining equity as a deposit on another PCP deal.

Under both PCP and contracts for deed, you accumulate no equity until the very end. With PCP, you're paying off depreciation, not principal; the car remains the finance company's asset until you make that final balloon payment, which around 80% of customers never do.

Both structures involve inflated prices to captive buyers. Contract sellers marked up properties dramatically to people who couldn't access normal mortgages. PCP dealers inflate list prices knowing buyers focus on monthly payments rather than not total cost.

Both run on a churn model. Lou Fushanis would evict, repossess, and resell the same property three or four times. PCP dealers push customers into new contracts before the old one ends, capturing them in perpetual payment cycles.

PCP, much like the contract for deed, punishes poor people for being poor; but this is just the Sam Vimes Theory of Socio-Economic Unfairness. Poor people have to pay more to borrow money; this is how capitalism works. If you think these contracts are unfair, you are not an antiracist; you are a social campaigner looking to devise a more equitable economic system.

So the particular crime committed against Clyde Ross was redlining; the rest is what happens to people locked out of mainstream credit. Coates conflated the two, overstating the case for slavery-specific reparations and understating how badly America's post-Depression credit system served the poor. The dysfunction was capitalist dysfunction; and reformers must reckon with it as such.